“Keep 6 months of expenses saved up.” You’ve heard this a hundred times. But for most Indian families, that number is dangerously low.

Every personal finance article will tell you to build an emergency fund. Very few will tell you how to actually calculate yours – not a generic number, but one that accounts for your EMIs, your dependants, your job stability, and the fact that you might be the only earning member in your family.

That’s what this post does. No generic advice. Just the math.

Why the “6 months expenses” rule doesn’t work for most Indians

The 6-month rule comes from Western personal finance, where dual-income households are the norm, healthcare is usually employer-covered, and parents typically don’t depend on their children financially.

In India, the picture looks very different:

You might be the sole earner supporting parents, a spouse, and kids. Your EMIs don’t pause when your income does – miss two home loan payments and you’re dealing with penalties and credit score damage. Health insurance gaps mean one hospitalisation can cost 3-5 lakhs out of pocket even with a policy. And if you lose your job, the average time to find a comparable role in India at the mid-senior level is 3-6 months, sometimes longer.

Six months of expenses assumes none of this complexity. For a lot of Indian families, it’s a starting point, not a target.

The actual formula

Here’s how to calculate your real emergency fund number:

Step 1: Calculate your monthly survival expenses

This is not your total monthly spending. It’s what you absolutely cannot avoid paying if your income stopped tomorrow:

- Rent or home loan EMI

- All other EMIs (car, personal loan, education loan)

- Groceries and household essentials

- Utility bills (electricity, water, gas, internet, phone)

- School/college fees if you have kids

- Insurance premiums (health, term – don’t let these lapse)

- Any regular payments to parents or dependants

- Basic transport

Leave out the discretionary stuff – dining out, subscriptions, shopping, vacations. You’d cut those immediately in a real emergency.

Step 2: Multiply by your coverage months

This is where it gets personal. The number of months you need depends on your situation:

6 months – Dual income household, no EMIs or very low EMIs, both partners in stable industries, no dependent parents

9 months – Single income household OR high EMI load (above 30% of income) OR dependent parents OR you work in a cyclical/volatile industry (startups, media, events, real estate)

12 months – Single income AND high EMIs AND dependants AND unstable industry. Also if you’re self-employed or freelancing.

If more than two of those risk factors apply to you, lean towards the higher end.

Karthik Rangappa from Zerodha Varsity puts it well in his video on emergency funds — the right number isn’t what some formula tells you. It’s the number that lets you and your family sleep at night. The framework above gives you a starting point, but if your gut says you need more, trust that. He also makes a great point about never parking your emergency fund in stocks or equity mutual funds. Worth a watch if you’re just starting out.

Step 3: Subtract what you already have

Add up your current liquid savings – the money you can access within 48 hours without penalties. This includes savings account balance, liquid mutual funds, and FD that you can break without significant loss.

Do NOT count: stocks (they can be down 30% when you need them), PPF (locked), real estate, gold jewellery you’d never actually sell, money you’ve lent to people.

Emergency fund gap = (Monthly survival expenses × Coverage months) – Current liquid savings

That gap is the number you’re working towards.

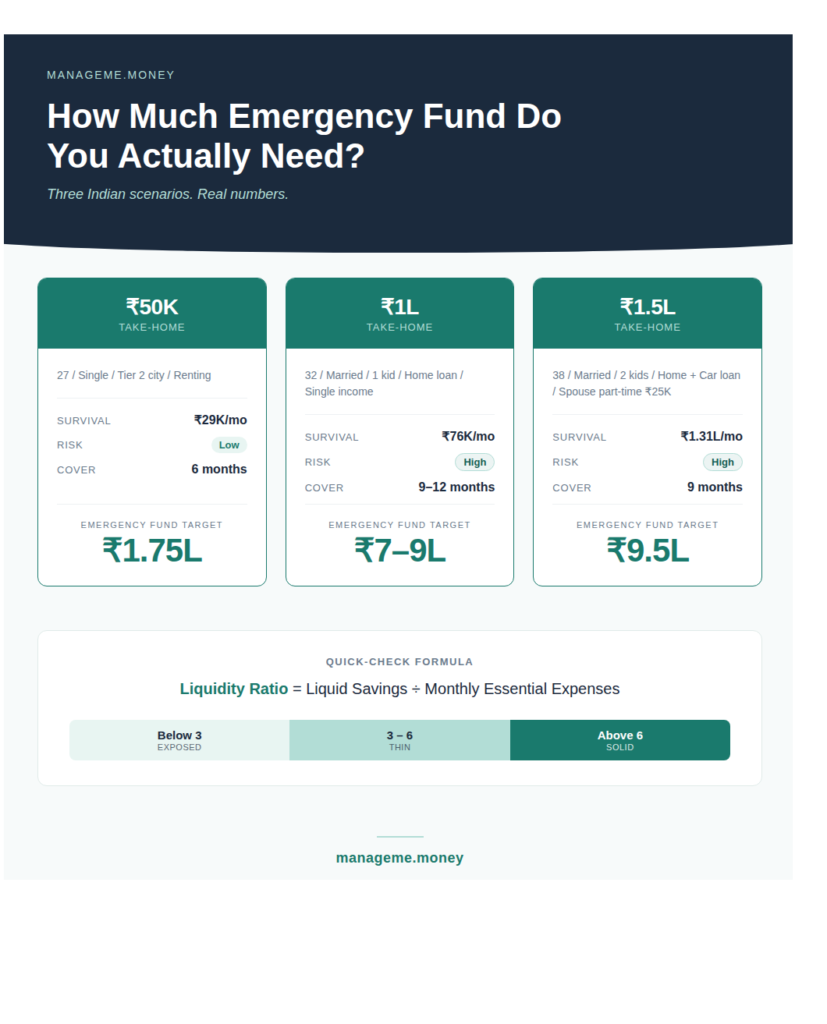

Worked examples with real Indian numbers

Let me run this for three different income levels so you can see how it plays out.

Example 1: Take-home ₹50,000/month

Situation: 27-year-old, renting in a Tier 2 city, single, no dependants, one personal loan EMI

Monthly survival expenses:

- Rent: ₹12,000

- Personal loan EMI: ₹5,000

- Groceries + utilities: ₹8,000

- Insurance premiums: ₹1,500

- Transport: ₹2,500

- Total: ₹29,000

Risk assessment: Single income, low EMIs, no dependants = 6 months

Emergency fund target: ₹1,74,000 (roughly ₹1.75L)

Not a terrifying number. Very achievable if you save ₹10K/month for 18 months. The mistake most people at this income make is thinking they’ll “start saving when they earn more.” Your expenses grow with your income. Start now.

Example 2: Take-home ₹1,00,000/month

Situation: 32-year-old, married, one kid, home loan, spouse not working, parents partially dependent

Monthly survival expenses:

- Home loan EMI: ₹32,000

- Groceries + household: ₹15,000

- Utilities + internet + phones: ₹5,000

- Kid’s school fees: ₹6,000

- Insurance premiums: ₹4,000

- Support to parents: ₹10,000

- Transport: ₹4,000

- Total: ₹76,000

Risk assessment: Single income + high EMI (32% of take-home) + dependants = 9-12 months

Emergency fund target: ₹6,84,000 to ₹9,12,000 (roughly ₹7-9L)

This is where most Indian families realise the gap. You’re taking home ₹1L but your non-negotiable outflow is ₹76K. Your actual monthly surplus is just ₹24K. And of that, you’re supposed to invest, handle unexpected expenses, AND build a 7-9L emergency fund.

This is exactly why the standard “6 months” advice falls short. At 6 months, this family has ₹4.56L saved. Sounds decent until you realise a job loss lasting 8 months (not uncommon at mid-career levels) leaves them short by ₹1.5L+ and staring at a personal loan.

Example 3: Take-home ₹1,50,000/month

Situation: 38-year-old, married, two kids, home loan + car loan, spouse works part-time earning ₹25K, parents fully dependent

Monthly survival expenses:

- Home loan EMI: ₹48,000

- Car loan EMI: ₹12,000

- Groceries + household: ₹20,000

- Utilities: ₹7,000

- Kids’ school fees: ₹18,000

- Insurance premiums: ₹6,000

- Parents’ expenses + medical: ₹15,000

- Transport: ₹5,000

- Total: ₹1,31,000

Risk assessment: Spouse earns but part-time (not stable) + high EMI (40%) + heavy dependants = 9 months (spouse income provides partial buffer)

Adjusted calculation: If spouse’s ₹25K continues, monthly gap during emergency = ₹1,31,000 – ₹25,000 = ₹1,06,000

Emergency fund target: ₹9,54,000 (roughly ₹9.5L)

Notice something? This family earns ₹1.75L combined but their survival burn rate is ₹1.31L. The lifestyle that felt comfortable on two incomes becomes extremely fragile if the primary income stops. And with an EMI-to-income ratio of 40%, they’re already in the danger zone we wrote about in our financial health check post.

Where to keep your emergency fund

This matters more than people think. Your emergency fund is not an investment. It has one job: be there when you need it, instantly, without losing value.

Best options for most people:

- High-interest savings account (some banks offer 6-7% on balances above ₹1L)

- Liquid mutual funds (can redeem within 24 hours, slightly better returns than savings account)

- A mix of both – keep 2 months in savings account for instant access, rest in liquid funds

Don’t use for emergency fund:

- Fixed deposits with lock-in (premature withdrawal penalties eat your returns)

- Debt mutual funds with exit loads

- Stocks or equity mutual funds (your emergency fund shouldn’t be down 20% the month you need it)

- PPF, NPS, or anything you can’t access within 48 hours

The one number that tells you where you stand

If you want to skip the full calculation and just get a quick read, there’s a simpler ratio.

Liquidity ratio = Liquid savings ÷ Monthly essential expenses

If the result is below 3, you’re financially exposed. One serious emergency and you’re borrowing. Between 3 and 6, you have a buffer but it’s thin. Above 6, you’re in a solid position for most situations.

This is one of the 16 ratios in a proper financial health check – and honestly, for most people, it’s the most important one to fix first. Before investments, before tax saving, before everything else. Because every other financial plan falls apart if you don’t have this foundation.

What to do right now

Calculate your monthly survival expenses. Just the non-negotiables. It’ll take 10 minutes with your bank statement open.

Multiply by your coverage months (6, 9, or 12 based on your situation above).

Compare that to your current liquid savings.

The gap is your target. Even if it takes 18-24 months to get there, you now have a real number instead of a vague intention to “save more.”

If you want the exact calculation done for you – including your liquidity ratio and how it compares to benchmarks for Indian families at your income level – our free financial health assessment covers this along with 15 other ratios. Takes about 30 minutes.

Or do the math yourself. The formula is right here. Either way, know your number.

Disclaimer: I’m not a certified financial planner – just sharing from personal experience, not financial advice. I built a financial health assessment tool, so I tend to nerd out on this stuff.

If you want to understand where you stand financially — not just your debt, but across 16 different financial ratios including your EMI-to-income ratio, savings rate, and emergency fund coverage — you can try our free financial health assessment. It takes about 30 minutes and gives you a clear picture of what needs attention first.